COVID-19 Information Hub – Financial Guidance

The information hub is no longer being managed. Due to this the links have been disabled.

Summary of Federal Government Stimulus Packages from our partner Cornwalls

As you will be aware, the federal government has announced two stimulus packages over the last week, aimed squarely at assisting the business community. The following is a summary of those measures.

Please note that we are working off the announcements themselves. There appear to be ongoing changes as the federal government seeks to better target its own measures. Therefore, the legislation itself may not strictly reflect the announcements.

What is clear is that this is a genuine attempt by Canberra to economically stimulate the business community and / or prevent a substantial increase in the unemployment rate in Australia.

We believe that overall, these measures are beneficial to business - especially those with a turnover of up to $50 million. It is certainly worth reviewing the measures and determining which parts of the stimulus packages may apply to you.

In addition, the speculation is that, in time, the federal government may announce a third tranche of measures in order to further stimulate the economy during the period of the COVID-19 pandemic.

We now turn to the measures announced to date.

The stimulus packages aim to assist small business entities (SBEs) by providing cash flow in the short term. For the purposes of this article, an SBE is a small to medium business entity with an aggregated annual turnover under $50 million.

The IAW threshold will increase from $30,000 to $150,000. Businesses with aggregated annual turnover of less than $500 million (up from $50 million) will be eligible for the IAW until 30 June 2020. This will apply on a per asset basis up to $150,000 exclusive of GST. The benefit of the IAW application on a per asset basis is that it enables eligible businesses to write-off multiple assets.

This incentive will only be available for assets first used, installed or acquired from 10:30am AEDT 12 March 2020 until 30 June 2020.

A time-limited 15 month investment incentive (expiring on 30 June 2021) will be introduced in order to support business investment and economic growth by accelerating depreciation deductions. Under this measure, businesses with aggregated turnover below $500 million will be able to immediately deduct 50% of the cost of an eligible asset on installation. Existing depreciation rules will apply to the balance of the asset’s cost.

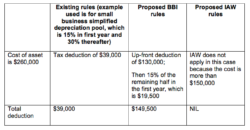

Below is a table that illustrates the IAW and BBI deduction amounts in the first year of acquisition, as compared to the existing small business simplified depreciation pool rules, using an asset with a cost of $260,000.

Not-for-profits and SBEs will receive a tax credit of $100,000, with a minimum credit of $20,000. Eligibility will be based on the prior financial year turnover. The payment will be delivered by the ATO as an automatic credit in the activity statement system from late April 2020, upon employers lodging eligible upcoming activity statements.

Eligible employers that withhold tax to the ATO on their employees’ salary and wages will receive a payment equal to 100% of the amount withheld, up to a maximum payment of $50,000 based on the March 2020 BAS.

Eligible employers that pay salary and wages will receive a minimum payment of $10,000, even if they are not required to withhold tax.

For quarterly lodgers, eligible businesses will be entitled to a maximum of $50,000 credit payable in late April 2020. The second eligible credit to a maximum of $50,000 will be payable in two instalments to a maximum of $25,000 each in the June and September 2020 BAS lodgements.

For monthly lodgers, eligible businesses will be entitled to a maximum if $50,000 credit payable in either, (depending on their specific circumstances) in late April 2020 in full, or during the June 2020 quarter subject to the application of the monthly PAYG / BAS credit formula in these rules.

Withdrawals of up to $10,000 will be available from April 2020 until 1 July 2020 for those eligible for the coronavirus supplement payment, as well as sole traders whose hours or income has fallen 20% or more as a result of the coronavirus. Eligible individuals will also be entitled to access up to an additional $10,000 from 1 July 2020 for approximately three months (the exact timing will depend on the passage of the legislation).

Superannuation minimum drawdown requirements for account-based pensions and similar products will be reduced by 50% for the 2020 and 2021 income years. This will benefit retirees by providing more flexibility as to how superannuation assets will be managed during this volatile period.

The federal government has set aside $1 billion to support regions and communities disproportionately affected by the economic impacts of COVID-19. This support includes those areas that are heavily reliant on tourism, agriculture and education. On a case by case basis, the Australian Taxation Office (ATO) will look to provide administrative relief for those who are directly affected by the virus.

The ATO has announced some specific concessions that may be available, including:

- deferring the payment date of amounts due through the BAS (including PAYG instalments), income tax assessments, fringe benefits assessments and excise for a period of up to four months;

- allowing businesses on a quarterly reporting cycle to elect to report monthly for GST purposes to obtain quicker access to GST refunds;

- allowing businesses to vary PAYG instalment amounts to zero for the April 2020 quarter. Businesses that vary their PAYG instalment to zero can also claim a refund for any instalments made for the September 2019 and December 2019 quarters;

- remitting any interest and penalties, incurred on or after 23 January 2020, that have been applied to tax liabilities; and

- working with affected businesses to help them pay their existing and ongoing tax liabilities by allowing them to enter into low interest payment plans.

The federal government will provide a guarantee of 50% to SBEs for new unsecured loans to be used as working capital. The government will provide eligible lenders with a guarantee for loans with the following terms:

- maximum total size of loans of $250,000 per borrower;

- loans of a three-year duration, with an initial six-month repayment holiday; and

- loans will be unsecured.

This scheme will commence by early April 2020 and will be made available for new loans made by participating lenders until 30 September 2020.

Small businesses will be able to apply for a wage subsidy of 50% of the apprentice’s or trainee’s wage, paid for up to nine months and commencing 1 January to 30 September 2020. The maximum subsidy amount is $21,000 per apprentice or trainee, or $7,000 per quarter per apprentice or trainee. This subsidy will only be available for businesses employing fewer than 20 full-time employees, and where the apprentice or trainee has been in training with the business from 1 March 2020.

Employers can register for the subsidy from April 2020 and claims for payment must be lodged by 31 December 2020.

Legislation to give effect to these measures will be introduced into Parliament, which resumes on 23 March 2020. It will be imperative for SBEs to consider these incentives so that action can be taken as soon as practicable.

For any advice or assistance regarding these incentives, please contact your Cornwalls representative or someone from the Cornwalls Tax team.

This article is general commentary on a topical issue and does not constitute legal advice. If you are concerned about any topics covered in this article, we recommend that you seek legal advice.

This article is current as of the time it was sent.

Federal Government’s COVID-19 Economic Stimulus Package

Read the Government’s Overview – Economic Response to the Coronavirus

Increasing the Instant Asset Write-off

Increasing the instant asset write-off for investments up to $150,000 (a 5-fold increase) made before 30 June 2020, for businesses with a turnover of less than $500 million (a ten-fold increase).

more info here

Accelerated depreciation deductions

Providing businesses with a 50% depreciation deduction in the year of installation for eligible assets purchased up to 30 June 2021, with existing depreciation rules applying to the balance of the asset’s cost.

more info here

Boosting cashflow for employers

Grants of between $2,000 and $25,000 for SMEs with turnover up to $50 million, to assist with cashflow the needed to maintain operations and to continue to employ staff.

read more here

Supporting apprentices and trainees

Wage subsidies of up to 50% of an apprentice’s and trainee’s wage for up to 9 months from 1 Jan to 30 Sept 2020, up to a maximum of $21,000 per apprentice/trainee. Where an employer is not able to retain an apprentice, the subsidy will be available to the new employer of the apprentice.

read more here

One-off direct payment of $750 to social security (i.e. pensioners and NewStart recipients), veterans and other income support recipients (i.e. farm household allowance).

This is targeted at those on the lowest disposable income that are the most likely to spend any increase in income immediately. It will give them the confidence to spend now rather than save, providing a direct stimulus - particularly to small business and the retail sector, where the bulk of this money will be spent.

$1 billion to support regions worst affected by the economic impacts of CoViD19.

This will include a waiver of fees and charges for tourism businesses accessing national parks and other Federal Government administered sites.

It also includes assistance to affected businesses, including those relianton tourism, agriculture and education, to identify alternative export markets or supply chains. This will encourage businesses to diversify beyond China, which currently represents between a third and half of international demand in these sectors.

Additional, targeted measures will be developed to further promote domestic tourism, suggesting an expansion of the advertising and

marketing program begun following the bushfires.

The ATO is also providing administrative relief for some tax obligations, on a caseby-case basis, with dedicated staff specialising in assisting small business.